You get a pay stub every two weeks.

But when’s the last time you actually read it?

If you don’t understand your pay stub, you could be:

Here’s what to look for (and why it matters):

Your pay stub generally includes:

Let me breakdown each part and what you need to think about:

With a $300,000 annual salary and 24 pay periods, your regular gross pay is:

Then let’s say you get a $100,000 bonus that will appear once per year.

This is typically seen in a dedicated "Bonus" earnings line.

Oftentimes, that bonus will be taxed differently and often more heavily, which we’ll cover later.

You may also see things like:

What Are Pre-Tax Deductions?

These are deductions taken from your gross pay before taxes are calculated. They reduce your taxable income, which in turn reduces how much you owe in federal income tax, state income tax, and FICA (Social Security + Medicare)—though some deductions only affect income tax, not FICA, like your 401() contributions.

Make sure you are looking throughout the year to see what has gone into:

That way you ensure you get them maxed out before year end. I see so many people leave thousands on the table because they did not look.

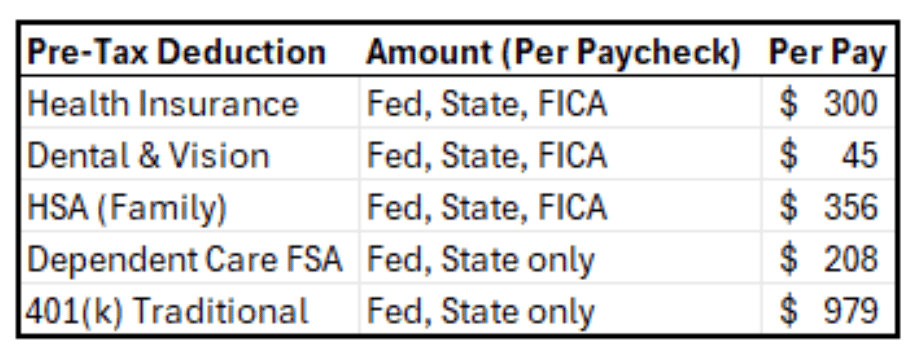

Common Pre-Tax Deductions (With Annual Limits for 2025)

Key Point: These deductions are subtracted before taxes are calculated, so they effectively reduce your taxable wages, not your gross pay.

Example Breakdown (Per Paycheck)

Assuming full participation:

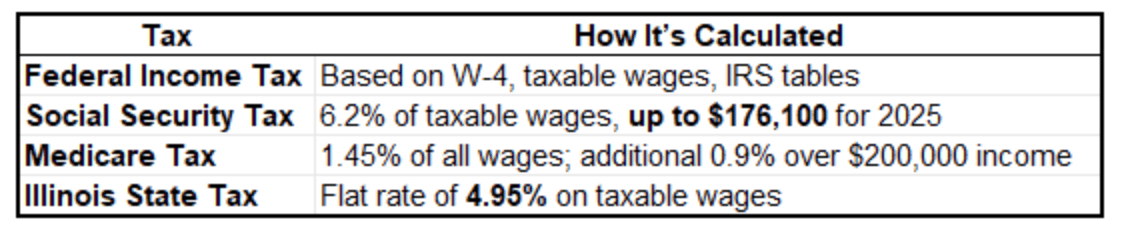

Your pay stub will break out these mandatory withholdings:

This is an area that you need to look at.

Divide your total fed withholding by your income and see what rate that is. If you are a high earner like most of my clients making $750k+ and that rate is 15-20%, you may have some issues and may need to pay quarterly taxes.

In this section, you can also look and see something most times called stock offset. This is the amount of shares that were sold to cover taxes on your RSUs. What percent was this? If 22%, you may be underwithholding here as well.

Bonus and RSU Note: When your bonus is paid, it may be taxed using a flat supplemental rate:

So your bonus and your RSU vests will be taxed at a lower rate than your regular pay. If you have a lot of other income, this can lead to underpayment penalties or a large tax bill at the end of the year. Be aware of your tax payments and withholding throughout the year.

These come after taxes are applied.

Mega Backdoor Roth 401(k)

This strategy allows you to contribute after-tax dollars to your 401(k) beyond the $23,500 pre-tax limit—up to a combined $70,000 total (employee + employer + after-tax contributions).

Example:

This will show up on your pay stub as:

This is also where you will see things like ESPP where you buy company stock, most times at a discount.

These are not deducted from taxable wages, but they still reduce your take-home pay.

Your pay stub may include the value of employer-paid perks:

These don’t affect take-home pay but are part of your total compensation and taxable income.

These are part of your total compensation even if they don’t show in your net pay.

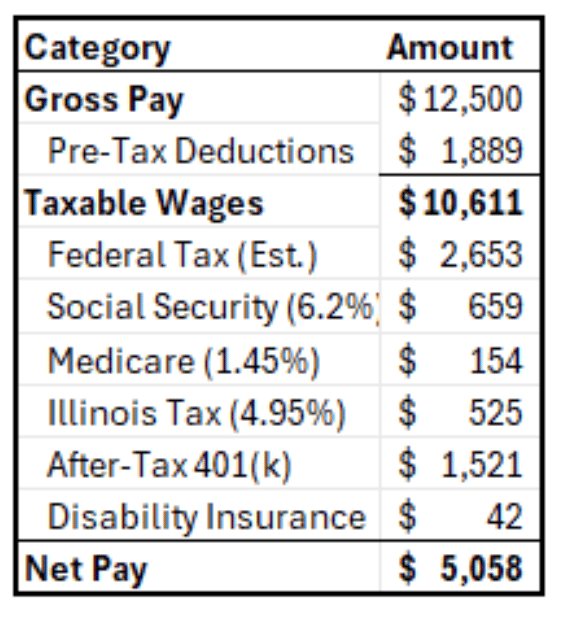

Once all deductions and taxes are applied, what’s left is your net pay—the amount that hits your bank account.

For example:

This is the key to it all.

Always check YTD sections for:

Make sure you or someone on your financial team are reviewing your paystubs on a regular basis and nothing is being left on the table!

Financial Advisor