For most of our lives, we’re taught basic money principles like “don’t spend too much,” “avoid debt,” and “always save for a rainy day.”

And that’s fine, when you’re getting started.

But once your income rises significantly, the old rules start to fall apart

Here are 12 money beliefs that high-income earners need to unlearn (and what to understand instead).

1) Savings rate is what matters

Yes, your savings rate matters. But at higher income levels, the efficiency of your dollars matters more.

You do not want to just aimlessly save in cash. This leads to less growth and higher taxes.

You need to focus on your investment rate.

Key point, it’s not just about saving more, it's about saving smarter and putting your dollars to work in the right places.

2) You need to buy a home

Homeownership is not a financial requirement, it's a personal decision.

For high earners, flexibility can be a financial superpower. Locking up a huge portion of capital in a primary home might limit your ability to invest elsewhere, especially in your early wealth-building years. The "renting is throwing money away" line doesn’t always apply at your level.

If you are going to be owning for a short period of time, it rarely is better than renting.

If you will stay there for 10-30 years, then oftentimes it will be better. But not by as much as you think.

3) Starting a business is too risky

Most of us were told this by our parents.

But starting a business has never been less risky. There are so many people succeeding at running solo businesses and doing the same thing they were doing before (think marketing, website design, social media, etc.)

Do not be scared to take your risks, especially at younger ages. It can be the fastest path to wealth.

4) I should only spend money on what I need

Early on, money is all about doing what is optimal and paying for what you need.

But at some point, the goal of money isn't just survival, it's quality of life.

If you're consistently under-spending out of guilt or fear, you’re not actually winning with money. Learn how to spend in ways that align with your values and make your life better, not just leaner.

You can buy things you want. You can outsource parts of your life that you do not like to do.

Use your money well!

5) Investing is too risky

I have heard this more and more lately from people. And they always have a story about how someone in their family lost it all.

Sure, gambling on a few stocks can be extremely risky, but that is why owning the world through index funds can make sense.

Over long time horizons, not being invested is one of the biggest wealth destroyers.

Sitting in cash might feel “safe,” but inflation quietly eats your money. Risk can’t be eliminated, it must be managed.

The longer you have to invest, the less risky it becomes.

6) You need to get out of all debt before investing

This is personal finance 101, but it’s not high-income finance.

If your income is strong and predictable, and your debt has low interest rates (like a mortgage or low interest car loan), you may be better off investing the extra dollars instead.

The math often favors building wealth, not just eliminating debt.

Especially when you are talking about a 401(k) with a match, Roth IRA, HSA, etc.

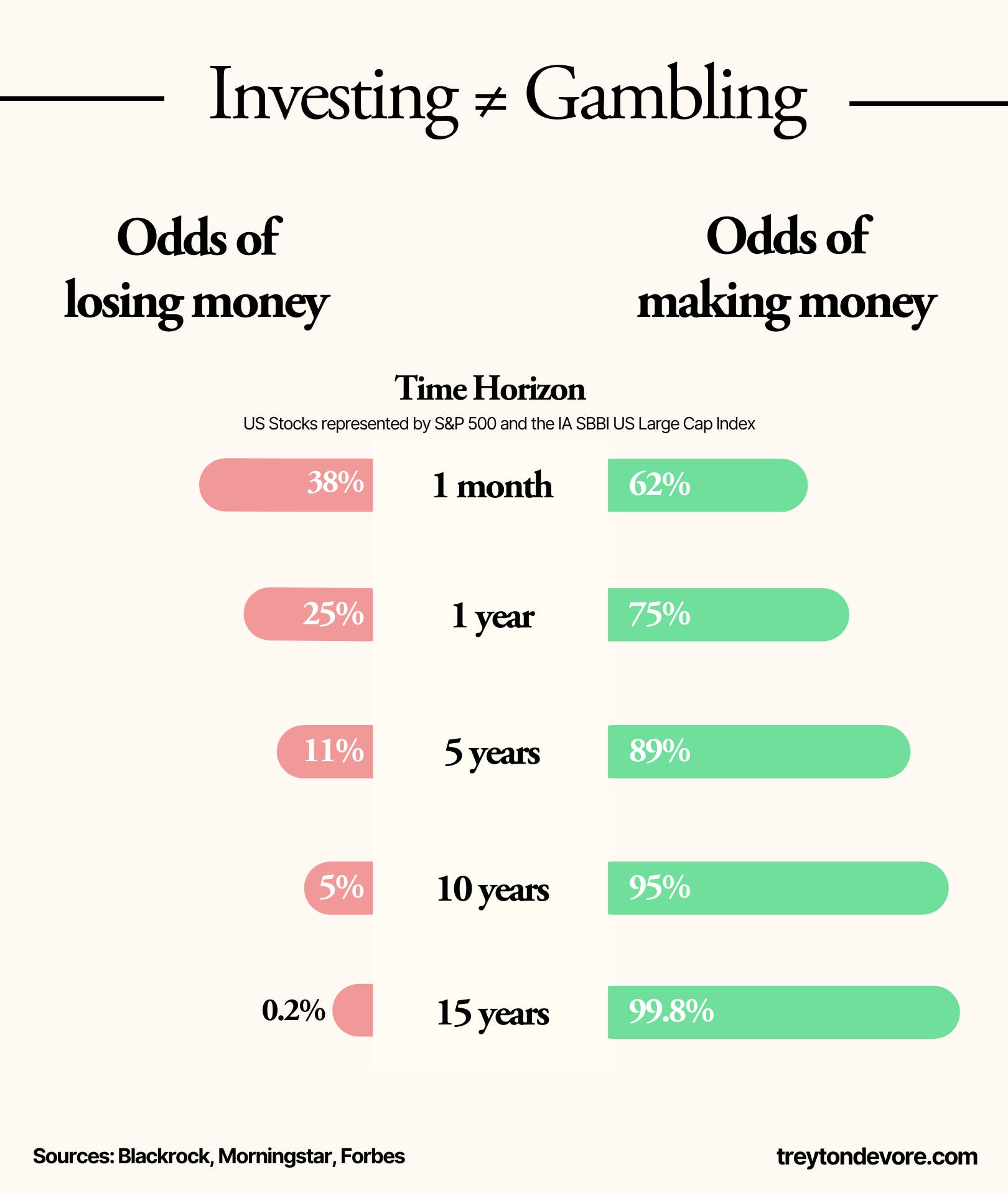

7) The stock market is like gambling

Gambling is guessing.

Investing is planning.

The market can feel unpredictable, but with the right strategy, you’re playing a game with long-term odds in your favor. Avoiding the stock market out of fear often results in missed growth and poor financial outcomes over time.

The goal is to get as much money invested for as long as possible.

That is how you win.

8) Insurance is not needed once you are wealthy

Wealth doesn’t remove risk, it often increases it.

As your net worth grows, so does your exposure.

Disability insurance, proper home and auto insurance. umbrella liability, and even life insurance (in some cases) remain essential tools to protect what you’ve built. Wealth is worth protecting.

You no longer need to worry about your phone breaking, a small car accident, etc.

It is all about protecting large outlays of cash.

9) More income always means more wealth

So many people believe this to be the case, but it is not true.

It is not about what you make, it is about what you keep.

So many end up spending everything they make, do not let this be you.

Always invest 20% of your income and make spending decisions from there.

10) I need a CPA who reduces my taxes as much as possible when they file

Tax planning happens during the year, not after.

Your tax team's job is to file according to what happened in the year.

Real tax planning needs to be done in the tax year to make any real moves.

Planning is where you save money.

11) My equity comp will take care of everything

Your equity comp can be your fastest path to wealth, but it can also destroy it.

You need to be wise on how much risk and concentration you take on with 1 individual stock.

The earlier the company, the more risk there is.

Make sure to be smart, plan around taxes, and take the right amount of risk while diversifying some throughout.

12) All student loan debt is good debt

Student loans can either be extremely smart or extremely dumb.

You do not want to take on $200,000 of debt to make $40,000.

But taking on $200,000 of debt to make $500,000 a year can make sense.

Make sure to help your children evaluate college in the right way.

These are 12 key topics that high income folks need to unlearn about money!

Financial Advisor