Fewer than 50% of people review their tax return.

Not because they don’t care, but because they don’t understand what they’re looking at.

Your 1040 tells a lot more than you think (if you know how to read it).

Here’s a simple breakdown of what every section means and what insights you can make from it:

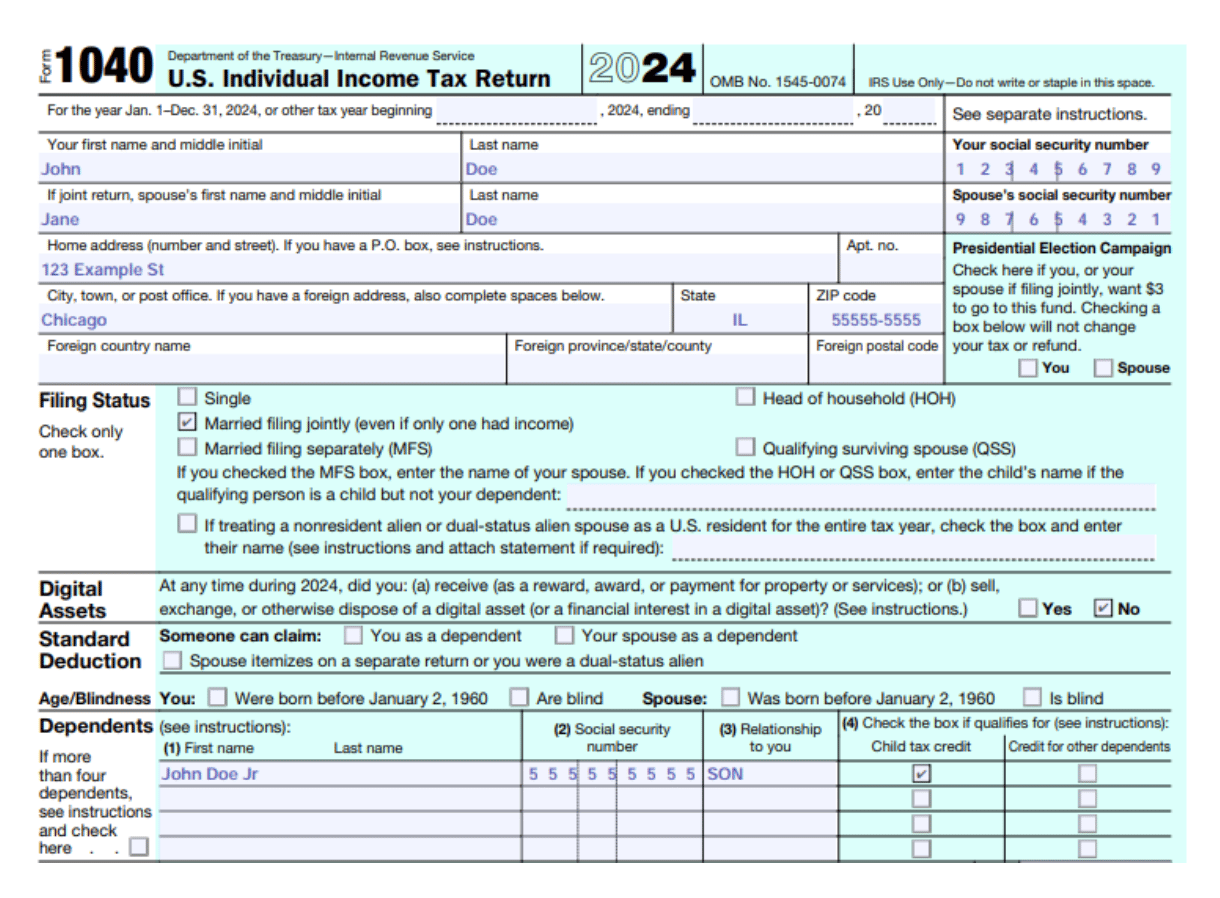

This section includes:

Filing status affects your tax rates and eligibility for certain credits. Dependents can qualify you for tax benefits.

There are not a ton of insights to grab from this section.

Just ensure:

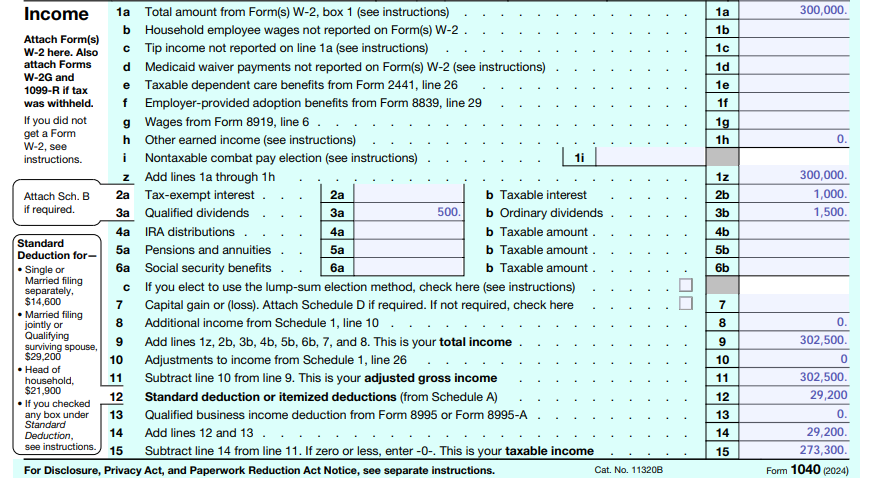

This summarizes the different types of income you received throughout the year:

This includes deductions like:

The result is your Adjusted Gross Income (AGI) (Line 11), a key figure used to determine eligibility for credits and deductions.

And then others like Roth IRA eligibility are calculated from your Modified Adjusted Gross income.

You need to be aware of both to ensure you can contribute to various accounts or what credits/deductions you are phased out of.

You either:

You should definitely know which you are taking.

If you take the standard, that means you did not have enough deductions from charity, state and local taxes, and mortgage interest to ‘beat’ the standard deduction. This means you do not benefit tax wise from those.

This could mean it makes sense to lump charitable donations, use a DAF, etc so you can take the standard some years and itemize in others.

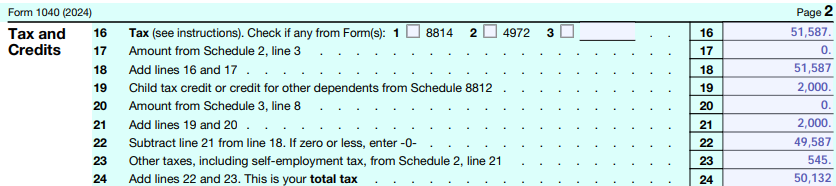

Page 2 of Form 1040: Deductions, Taxes, Credits and Balance Info

This section calculates your actual tax owed based on:

Line 24: Total tax owed after credits.

Make sure you take a look at this and understand what your tax liability is.

I would also encourage you to go calculate your effective tax rate (taxes/income made).

Remember, you may be in the 37% bracket, but not all income is taxed at 37%. Your effective rate is most important to know.

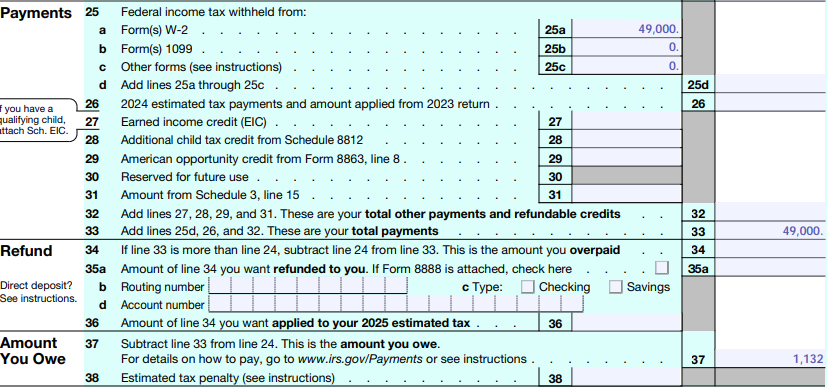

This includes:

This section is really important. It tells you what you paid in so you can compare it to what you owe.

If you paid in way too little, you probably have penalties (which you can go see on line 38).

Not paying penalties is low hanging fruit for most people.

You’ll also see bank account info here if you choose direct deposit.

For many business owners, or those who pay quarterly tax payments, it often makes sense to apply the overpayment to Q1. This is why I hate the idea that “you are giving the government an interest free loan” for high earners. It is not that deep, overpay some, apply to Q1, reduce what you pay in Q1, and move on.

Both you and your preparer (if applicable) must sign and date the return. If someone helped you file it, their info appears here too.

Even if you rely on a tax preparer, reviewing your Form 1040 can help you:

Even though a tax preparer files it, it is still you signing it and saying it is all correct. You would be the one in trouble if something is wrong, not them. So review it and learn from it!

And if you have an advisor, they should be reviewing every return of yours for mistakes and planning opportunities.

Financial Advisor